Patience Is the New Sexy

Why Financial Foreplay Beats Quick Cash Flings

Listen to a podcast-style discussion of this article or download it here

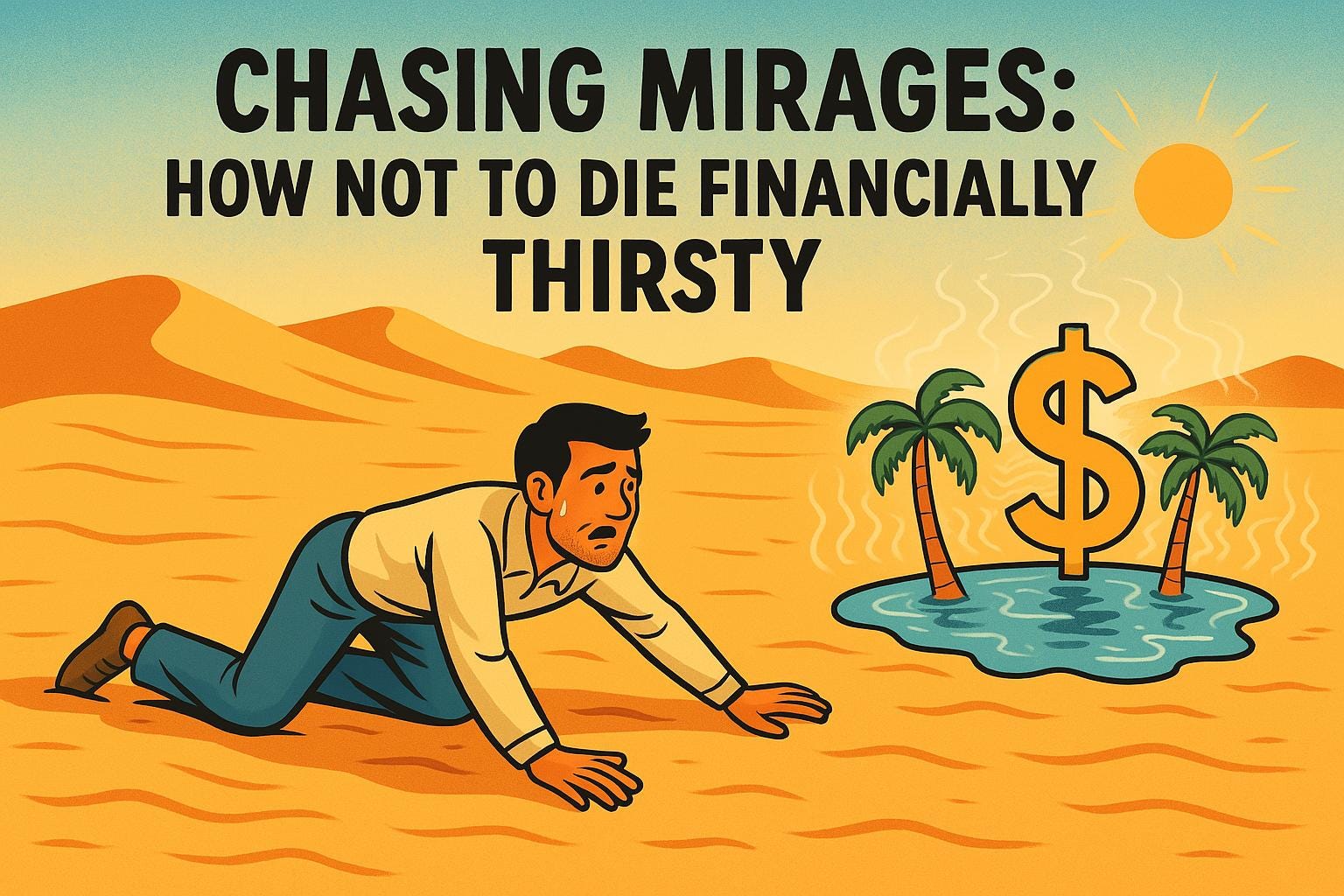

The sun beat down mercilessly on Ahmed's parched skin as he trudged across the endless dunes. His water supply had dwindled to mere drops three days ago, and desperation clouded his thoughts like the heat waves rippling across the horizon. His caravan had been separated during the sandstorm, leaving him alone to navigate the treacherous desert.

Just as hope began to fade, he spotted it—an oasis shimmering in the distance. Vibrant palm trees swayed gently, their reflection dancing on a pool of crystal-clear water. With renewed vigour, Ahmed altered his course, stumbling forward with newfound determination. For hours he walked, yet the oasis remained tantalizingly distant. As the sun began to set, casting long shadows across the sand, Ahmed realized the cruel truth: there was no oasis. What he had pursued so desperately was nothing but a mirage—an illusion created by heat, light, and his own desperate desire.

Exhausted and defeated, he collapsed onto the sand. But as fortune would have it, a real caravan discovered him at dawn. The leader, an old merchant named Karim, offered him water and shelter.

"What led you so far off the ancient trade route?" Karim asked.

Ahmed described the illusory oasis that had beckoned him away from the path.

The old merchant nodded knowingly. "The desert is full of such deceptions. The experienced traveller knows to follow the stars and the established paths, not chase after shimmering promises on the horizon. The journey is long, but the true oases exist only where patience and wisdom guide us."

Like Ahmed's mirage, the allure of instant wealth often appears as a shimmering promise on our financial horizon. We chase after it, sometimes abandoning proven paths in pursuit of an illusion. True financial abundance rarely manifests overnight. Instead, it emerges through the steady application of principles, patience, and perseverance.

The Allure of Instant Wealth

We live in a culture that celebrates overnight success and instant gratification. Social media feeds are filled with "rags-to-riches" stories: the college dropout who became a tech billionaire, the investor who turned $1,000 into $1,000,000 with cryptocurrency, the influencer who makes six figures a month "while sleeping." These narratives activate powerful psychological triggers that can override our rational thinking.

Psychological Triggers

Fear of Missing Out (FOMO) may be the most potent force driving our pursuit of quick wealth. When we see others apparently striking it rich through speculative investments or business ventures, a primal fear activates: what if this is my one chance to escape financial struggle, and I'm missing it? This anxiety is amplified by carefully curated social media content that highlights wins while concealing losses.

In 2021, the GameStop stock surge led many retail investors to experience significant financial losses. For instance, some individuals, inspired by the rapid gains shared on forums like r/wallstreetbets, invested their emergency savings into volatile meme stocks, only to see their investments plummet by as much as 70%

Greed and impatience form another powerful cocktail. The human brain evolved in environments of scarcity, wiring us to seize apparent abundance whenever possible. Combined with our modern impatience—fuelled by same-day delivery services and instant digital gratification—we become perfect targets for promises of rapid enrichment. We come to expect “now”, because in many cases we can get it now.

Cognitive biases further distort our decision-making. Hyperbolic discounting leads us to dramatically overvalue immediate rewards compared to future benefits, even when the future benefits are substantially larger. We tend to choose $100 today over $150 in six months, despite the 50% return being extraordinary by investment standards.

Confirmation bias causes us to seek information that supports our desire for quick wealth while ignoring cautionary evidence. Survivorship bias ensures we hear about the rare successes while the far more numerous failures fade into obscurity.

Real-Life Examples

The landscape of get-rich-quick schemes continues to evolve, from classic pyramid schemes to sophisticated digital frauds. Recent years have seen:

· "Investment education" programs charging thousands of dollars for "secret" trading strategies that rarely work in practice (subscribing to my newsletter is entirely free, just saying…)

· Cryptocurrency pump-and-dump schemes where influencers hype tokens before quietly selling their own holdings

· Dropshipping "masterclasses" promising six-figure incomes through minimal work

· Real estate seminars teaching "no money down" techniques that often rely on questionable lending practices

Cryptocurrency investment scams have led to significant financial losses for many individuals. For example, in 2024, a woman from St. Francis, Wisconsin, lost $80,000 after being lured into a fraudulent crypto investment scheme through an online advertisement . Similarly, the collapse of the Canadian cryptocurrency exchange QuadrigaCX in 2019 resulted in approximately C$215.7 million in liabilities, affecting around 115,000 customers.

The emotional toll of such scams often surpasses the financial damage. Victims commonly report feelings of shame, depression, and a lasting erosion of trust that impacts their future financial decisions. A study by the University of Cambridge revealed that fraud victims experience high levels of stress, anxiety, and depression due to the sense of violation and betrayal associated with the fear of new fraud. Additionally, many victims feel too embarrassed to report the crime, leading to underreporting and a lack of support.

The Reality: Wealth Accumulation Takes Time

Despite the allure of overnight riches, substantial evidence indicates that sustainable wealth typically develops through consistent effort over time.

Statistical Insights

According to research from the Ramsey Solutions National Study of Millionaires, 79% of American millionaires didn't receive any inheritance. Instead, they built their wealth primarily through consistent investing in employer-sponsored retirement plans over periods averaging 28 years. Nearly three-quarters of these millionaires listed regular, disciplined investing as a top factor in their financial success.

Data from numerous studies indicates that sudden wealth—whether through inheritance, lottery winnings, or unexpected business success—often dissipates quickly. The National Endowment for Financial Education suggests that about 70% of people who suddenly receive large sums of money will lose it within a few years.

Why? The skills, habits, and mindset required to maintain and grow wealth are typically developed during the process of acquiring it. Those who bypass this development through sudden windfalls often lack the necessary foundation for long-term financial management.

Case Studies

David became a millionaire not through a single brilliant investment but by what he calls "The Latte Factor"—saving small amounts consistently over time and allowing compound interest to work its magic. He calculated that saving just $5 daily (the cost of a coffee) and investing it at an 8% return would yield over $1.2 million after 40 years.

Jennifer and Daniel accumulated a net worth of $2.3 million by their early fifties despite never earning more than $95,000 annually combined. Their strategy? Maintaining a consistent 20% savings rate, maximizing employer 401(k) matches, purchasing modest real estate in up-and-coming neighbourhoods, and avoiding lifestyle inflation as their careers progressed.

"It wasn't one big decision that made the difference," Jennifer explained. "It was thousands of small choices over decades. We drove our cars for 15+ years. We took budget vacations. We celebrated promotions without upgrading our housing. None of these decisions felt significant at the time, but together they created our financial independence."

Strategies to 'Get Rich Quick(er)'

While overnight wealth remains largely mythical, certain approaches can accelerate your financial progress compared to average results. The key lies in reframing what "quick" means in the context of wealth-building.

Mindset Shift

Instead of seeking shortcuts that promise implausible returns, focus on optimizing proven wealth-building principles. Think of your financial journey not as a sprint but as a marathon where intelligent training and strategy can improve your finish time.

The first step is adopting what financial psychologists call an "abundance mindset with delayed gratification"—recognizing that significant wealth is indeed possible while accepting that it requires systematic effort over time.

Practical Steps

Automated Savings represent the foundation of accelerated wealth-building. By automating transfers to investment accounts immediately after receiving income, you circumvent the psychological friction that makes manual saving difficult. This approach leverages behavioural economics principles by making smart financial behaviour your default rather than requiring continuous willpower.

Research indicates that people who automate their finances save an average of 15% more than those who rely on manual transfers. Consider the case of Marcus, who automated 30% of his income toward investments when he began his career at age 22. By age 40, he had accumulated over $780,000 despite a modest $60,000 average salary.

Investing in Education delivers among the highest returns available. While pursuing formal degrees can be valuable, targeted skill development often provides faster financial returns. Data scientists who complete specialized bootcamps, for instance, report average salary increases of $25,000-$35,000. Similarly, sales professionals who invest in advanced negotiation training often see commission improvements of 20-30%.

Sarah, a graphic designer, invested $4,000 in UX/UI certification courses, which enabled her to transition into a role that paid $32,000 more annually. "That education paid for itself in less than two months," she noted, "and continues to generate returns years later."

Diversified Investments with appropriate risk allocation form another acceleration strategy. While maintaining a core portfolio of index funds provides stability, allocating a percentage to higher-growth opportunities can enhance overall returns. The key is ensuring these higher-risk investments represent money you can afford to lose.

Some financial advisors recommend what they call "the 80/15/5 approach" for those seeking accelerated growth: "Put 80% in broad-market index funds, 15% in targeted growth investments related to your professional expertise, and 5% in calculated speculative opportunities. This provides a solid foundation while allowing for the possibility of outsized returns."

Expert Opinions

Dr. William Bernstein, neurologist-turned-investment advisor and author of "The Four Pillars of Investing," emphasizes that most wealth-building occurs through saving rather than spectacular investment returns. "The financially successful," he notes, "are typically prodigious accumulators of capital, not investment geniuses."

Vicki Robin, co-author of "Your Money or Your Life," suggests that redefining "enough" represents the fastest path to financial freedom. By calculating your true hourly wage (after accounting for work-related expenses) and evaluating purchases based on "life energy" required to afford them, you naturally optimize spending and accelerate wealth accumulation.

Morgan Housel, author of "The Psychology of Money," observes that financial success depends more on behaviour than intelligence: "Financial outcomes are driven by your savings rate, how long you save, and your ability to stick with your strategy through market cycles—none of which require a high IQ."

Embracing the Journey

Like Ahmed in our opening parable, we face a choice in our financial lives: chase after mirages that promise quick relief but lead nowhere, or follow proven paths with discipline and patience.

The allure of instant wealth is understandable—who wouldn't prefer financial freedom today over freedom in ten years? Yet this desire, when channelled into unrealistic schemes, often delays or derails our progress toward genuine prosperity.

The wealthiest individuals I've come across share a common perspective: they stopped viewing wealth as a destination and started seeing it as a journey—a series of consistent actions aligned with long-term objectives. This mindset shift transforms financial management from a burden into a practice, much like meditation or exercise.

Consider:

1. Are your strategies based on evidence and reasonable assumptions, or on exceptional outliers?

2. Have you automated your wealth-building to ensure consistency despite fluctuating motivation?

3. Are you investing in developing rare and valuable skills that increase your earning capacity?

4. Have you built safeguards against your own behavioural tendencies toward FOMO and impulsivity?

While the journey to financial abundance may not be as quick as you'd hope, it's also not as slow as you fear when approached systematically. It’s hard to know exactly who originally came up with the idea (the computer scientist J.C.R. Licklider included a version of this concept in his book Libraries of the Future), but the journal maximum the people tend to overestimate what they can achieve in one year and tend to underestimate what can be achieved in 10 years, has certainly mean quoted by people like Bill Gates and many other notable visionaries. Combining proven principles with strategic optimization, you can accelerate your path to prosperity without chasing financial mirages across the desert.

Like the experienced desert traveller, the disciplined wealth-builder follows the stars and established paths rather than shimmering illusions on the horizon. The journey may be long, but the true oases—financial security, freedom, and peace of mind—await those guided by patience and wisdom.